A debt consolidation home loan does one simple thing: it rolls your expensive debts — credit cards, personal loans, car loans, buy-now-pay-later hangovers — into your mortgage, which charges a fraction of the interest. Done right, it can turn five painful repayments into one manageable one and free up serious monthly cashflow. Done lazily, it turns a 3-year car loan into a 30-year one. This guide covers both halves, because the second half is where people get hurt.

Drowning in repayments? Email startnow@sorenfinancial.com with a list of what you owe and we will map out whether consolidating stacks up for you.

How a debt consolidation home loan works

Your home loan is almost always your cheapest debt, because the bank holds your house as security. Cards and personal loans are unsecured, so they charge multiples of your mortgage rate. Refinancing to consolidate means increasing your home loan and using the extra to clear the expensive debts, so every dollar you owe is now charged at the home loan rate. With the cash rate at 4.35% and variable rates around the 6% mark, the gap between your mortgage and your card rate has rarely mattered more.

The trap: cheap debt held for decades is not cheap

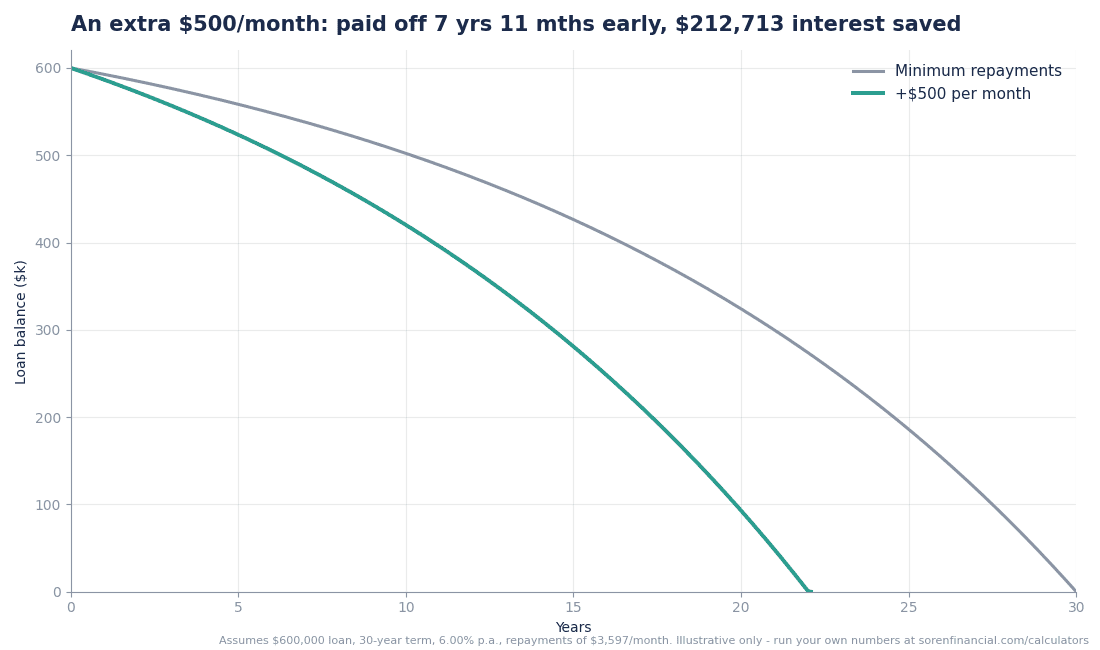

Here is the part the ads skip. Stretch a $20,000 debt over 30 years, even at a home loan rate, and you can pay more total interest than you would have on the original ugly rate over 3 years. The fix is simple and takes discipline: after consolidating, keep paying what you were paying before. If your old repayments were $1,500 a month across all your debts and your new consolidated repayment is $900, put the spare $600 into the loan as extra repayments. The chart above shows what that kind of consistent extra payment does — years off the loan and six figures of interest saved. Consolidation buys you breathing room; extra repayments make it a win.

Will the bank even approve it?

Lenders assess a consolidation refinance like any other application: income, expenses, equity and your repayment history, all stress-tested at your rate plus APRA’s 3% buffer. Recent missed payments make it harder, which is why the time to consolidate is before the wheels wobble, not after. If your position is tight, this is squarely a case for a broker — different lenders treat consolidation very differently, and we know which doors to knock on.

Is a debt consolidation home loan right for you?

Good candidates: stable income, real equity, multiple expensive debts, and the honesty to cut up the cards afterwards. Poor candidates: anyone planning to consolidate and then run the cards straight back up — that road ends with the same debts plus a bigger mortgage. If you recognise yourself in the first group, run your numbers on our calculators and check our refinancing tips for 2026 while you are at it.

Moral of the story: a debt consolidation home loan is a tool, not a magic wand — it works when the structure and the discipline both show up. Get in touch at startnow@sorenfinancial.com and we will tell you honestly which group you are in. Reviews on OurTop10.

About the author

Mansour Soltani

Founder and CEO, Soren Financial

Mansour leads Soren Financial, working with clients across home loans, refinancing and property investment. A regular media contributor to ABC, Domain and Australian Broker, he holds a Certificate IV and Diploma in Finance and Mortgage Broking.

View full profile →