Should I refinance my mortgage in 2026? With the cash rate back at 4.35% after three hikes this year, it is the right question — but the answer depends on which of two groups you are in. For one group, refinancing this year is close to free money. For the other, it is paperwork for nothing. Two minutes of reading will tell you which one you are.

Shortcut: email your current rate, balance and lender to startnow@sorenfinancial.com and we will tell you which group you are in by tomorrow.

Signs you should refinance your mortgage this year

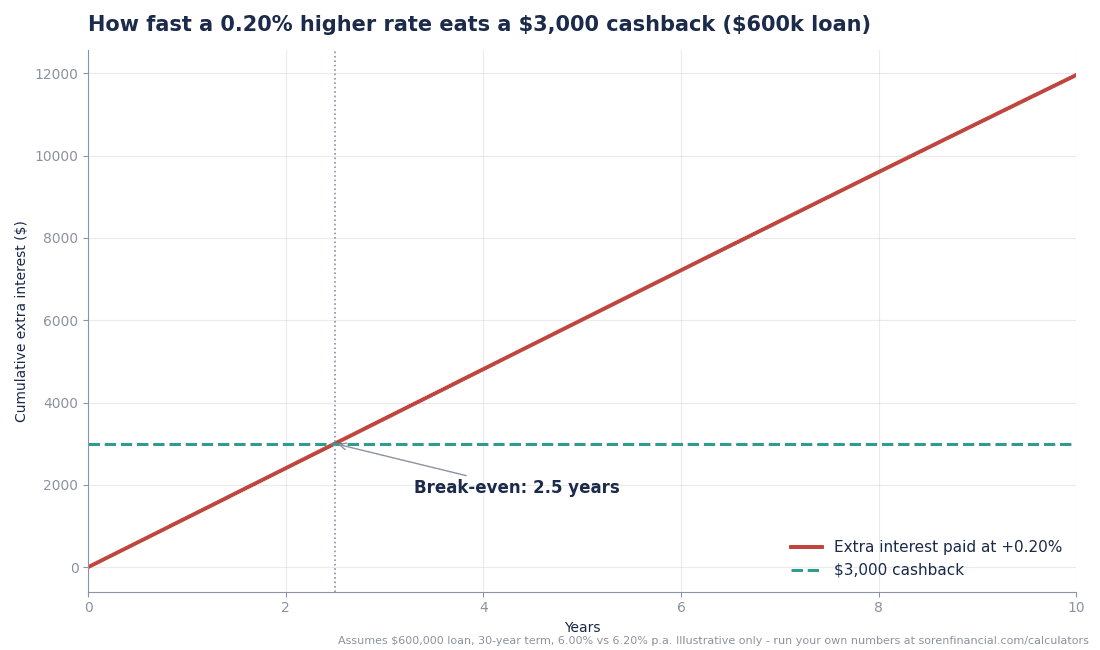

Your rate starts with a 6 and a big number after it. Your fixed term just ended and you are sitting on the revert rate (covered here). You have not touched your loan in 3+ years — the loyalty tax compounds quietly. Your property value has grown enough to drop your LVR a pricing tier. Or you are juggling expensive debts that belong consolidated into the mortgage. Any one of these usually pays for the effort; two or more and you are leaving real money on the table. The chart above shows the cost of ignoring even a 0.20% gap.

When refinancing is NOT worth it

Honesty corner: refinancing is not free money for everyone. If your balance is small or your remaining term short, the dollar savings may not beat the switching costs. If you fixed recently, break costs can eat years of savings — get them quoted before you decide anything. If you plan to sell within a year or two, or your income situation has deteriorated since you last applied, a refinance can cost more than it returns. A good broker tells you this before you apply, not after.

Should I refinance my mortgage now or wait for rate cuts?

The waiting-for-cuts strategy has a data problem: the OurTop10 Rate Prediction Index currently prices a 0% chance of a cut at the 11 August meeting, with a 22.3% chance of another hike. Meanwhile every month on an uncompetitive rate is money gone for good. Refinance to the sharpest deal available now; if cuts eventually come, a variable rate rides them down anyway. Our full playbook is in refinancing tips for 2026, and yes, a couple of lenders still pay cashbacks.

What it actually takes

A refinance in 2026 runs 2-6 weeks: application, valuation, approval, discharge and settlement. Your file gets fully reassessed — income, expenses, buffers at the new rate plus 3% — so come prepared. Most of the legwork is exactly what we do all day, which is the least shameless version of the shameless plug I can manage. Start with your numbers on our calculators.

Moral of the story: should I refinance my mortgage is answered by arithmetic, not anniversaries. If your rate, LVR or debts have moved since you last looked, get in touch at startnow@sorenfinancial.com. Client reviews on OurTop10.

About the author

Mansour Soltani

Founder and CEO, Soren Financial

Mansour leads Soren Financial, working with clients across home loans, refinancing and property investment. A regular media contributor to ABC, Domain and Australian Broker, he holds a Certificate IV and Diploma in Finance and Mortgage Broking.

View full profile →