With rising interest rates, is now the time to fix my home loan in 2026?

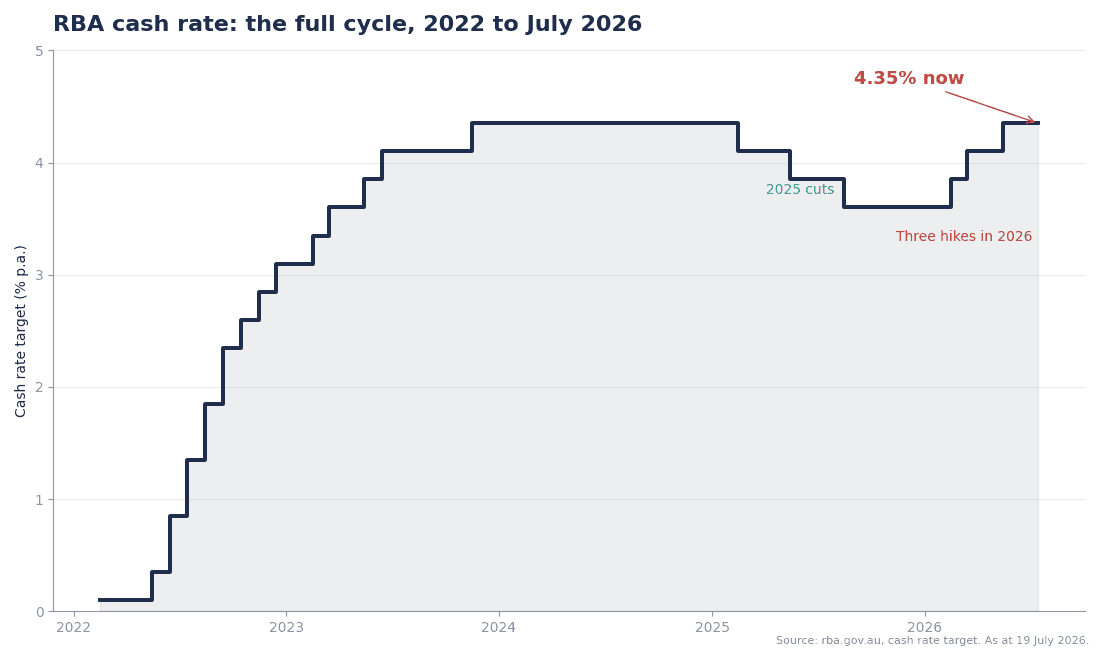

Here we go again. After the RBA cut rates through 2025, it has turned around and lifted the cash rate three times this year, and it now sits at 4.35%. The phones have started ringing the same way they did back in 2022, with the same question: should I fix my rate before it gets worse? The honest answer to “should I fix my home loan” is that it depends on your situation, and anyone who gives you a blanket yes or no isn’t doing you any favours. There are many variables (excuse the pun), so let’s cover the main ones off:

Want us to run the numbers on your loan instead of guessing? Reach out at startnow@sorenfinancial.com and we will review it for you.

How long should I fix my home loan for?

Well, if you are a “set and forget” kind of person who doesn’t want to think about rates for a while, a 1-2 year fixed term is where I would start the conversation. The cost of fixing for 4/5 years is still quite high. The main reason people want to fix for that period of time is peace of mind and also controlling your fixed costs for a term.

I get that however it needs to make financial sense as well, when you fix the banks have already added a margin into the rate so you need to run the numbers to make sure you are not paying too much for the privilege.

Fixed vs variable home loan: the argument in 2026

There are people who sit on either side of this argument, however if you look at this through the lens of “the bank is 5 steps ahead of you and will always win”, then the aim of the game is to reduce how much they win by and this is where your broker can help :).

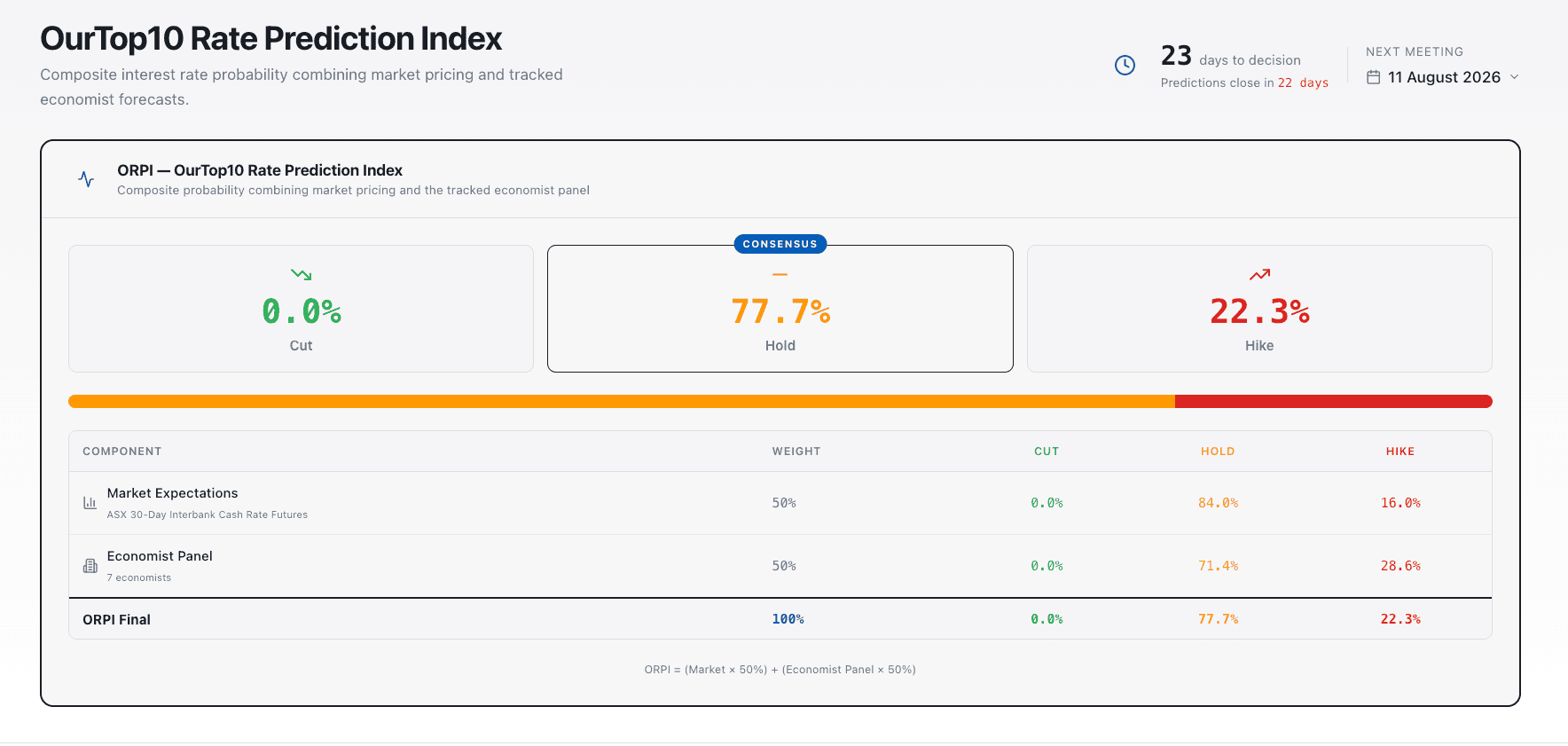

So where are rates actually heading? Rather than guessing, take a look at the OurTop10 Rate Prediction Index (ORPI), which combines ASX market pricing with a tracked panel of economists ahead of every RBA decision. Heading into the 11 August 2026 meeting, ORPI has it at a 77.7% chance of a hold and a 22.3% chance of another hike, with a 0% chance of a cut. Read that again: not a single signal is pointing to rates coming down at the next meeting. The economist panel is split 5 hold to 2 hike, and the market is pricing a 16% chance of another rise. ORPI has called 63 of the last 73 RBA decisions correctly since 2019, so while nobody rings a bell at the top, this is about as good a read as you will get. If there is still a 1-in-5 chance of another hike and no cut in sight, fixing part of your loan starts looking less like panic and more like planning.

So, should I fix my home loan for 5 years to counter rising interest rates?

The banks have already priced in your potential exuberance into the rates available at the 4-5 year mark, so there is rarely a real financial gain paying that margin for half a decade just to feel safe. If you genuinely can’t sleep at night on variable, there are better ways to get that certainty.

Thanks Captain Obvious, so what are you getting at?

There are other options available to you, other than fixing your rates. Some examples are:

- Splitting your loan. This is a great way to hedge your bets and give you peace of mind. Fix a portion of your loan and keep the rest variable with an offset working against it. Work out your average rate across the two and you could be getting a great deal by structuring your loan this way, without betting the whole house on one side of the argument.

- Use an offset account: Connect this account to the variable component of your loan. Have your salary placed into your offset and use this account to pay bills etc.

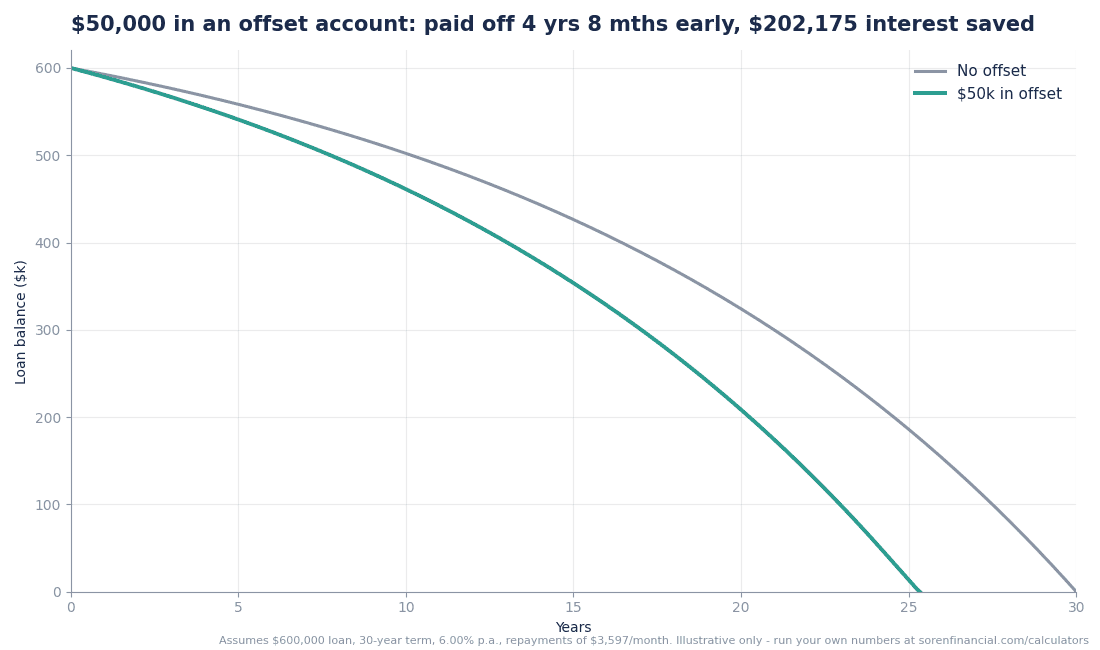

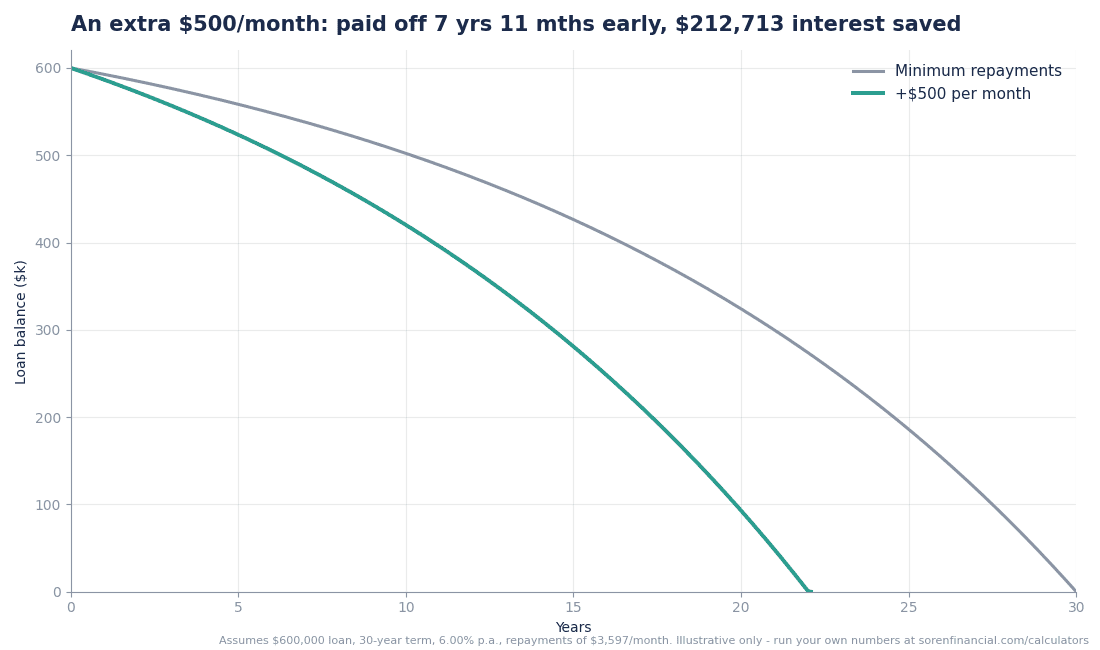

- Make extra repayments: take a look at the below graphs and see the difference for yourself

- Shameless Plug: Have a broker review your loans for you. You can read our client reviews on OurTop10, and get in touch at startnow@sorenfinancial.com

Take a look at these graphs which you can find on our website and see the years you save if you place 50k into an offset. At today’s rates you have wiped 4 years and 8 months off your loan and saved over $200,000 in interest

If you can add another $500 per month to your loan as an extra repayment, look at what happens, you save 7 years and 11 months and over $210,000 in interest

Moral of the story is that there are other ways to counter rising rates, go to our calculator section and see for yourself or even better get in touch and we will show you how you should be structuring your loan and preparing for whatever the RBA does next. Contact us at startnow@sorenfinancial.com to learn more.

About the author

Mansour Soltani

Founder and CEO, Soren Financial

Mansour leads Soren Financial, working with clients across home loans, refinancing and property investment. A regular media contributor to ABC, Domain and Australian Broker, he holds a Certificate IV and Diploma in Finance and Mortgage Broking.

View full profile →