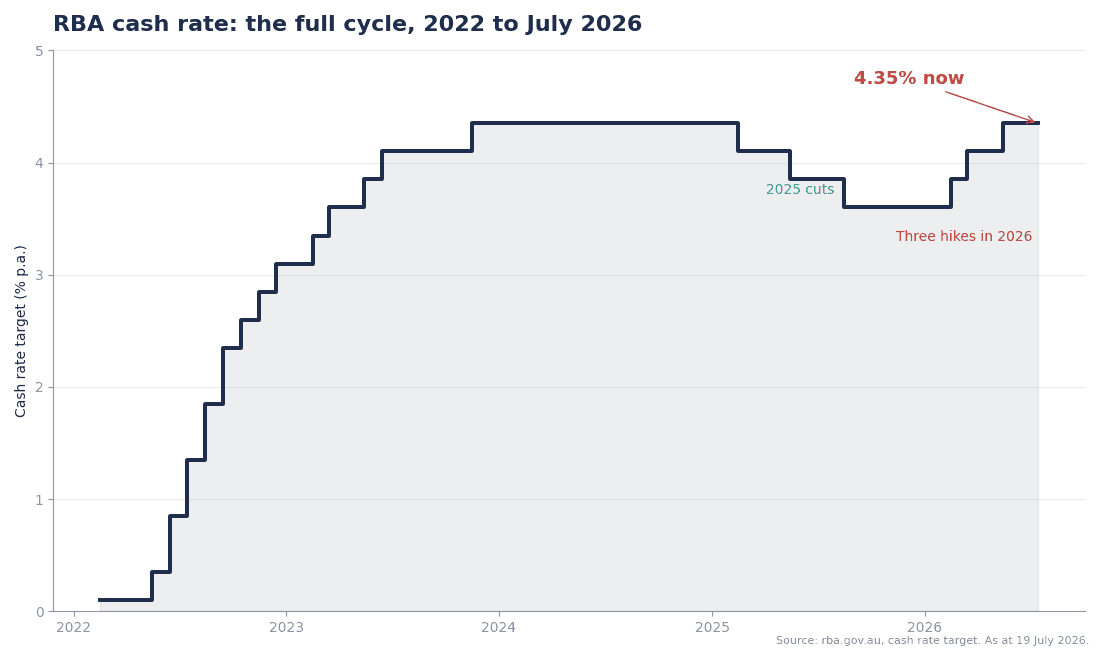

Remember the “fixed-rate cliff” headlines of 2023? The lesson from that whole episode never expired: a fixed rate ending is a scheduled event you can see coming for years, and yet most people still let it ambush them. With the cash rate back at 4.35% after three hikes this year, anyone rolling off a fixed term in 2026 is stepping into a very different rate than the one they locked. Here are the 5 things to know before your date comes up.

Fixed term expiring in the next 6 months? Email the date to startnow@sorenfinancial.com and we will build your exit plan before the bank builds theirs.

1. Know your revert rate — it is not a nice number

When your fixed rate ends and you do nothing, your loan “reverts” to a variable rate the lender chooses, and it is rarely their sharp one. Doing nothing is a decision, and it is usually the most expensive one available. Find your revert rate in your loan documents or ask us to pull it.

2. Start 3 months before your fixed rate ends

Repricing with your own bank takes a phone call; refinancing takes weeks. Start 3 months out and every option is on the table, including settling a refinance the same week your fixed term expires so you never spend a day on the revert rate. Start after it ends and you are negotiating from the back foot while paying the penalty rate.

3. Reprice first, refinance if they don’t play

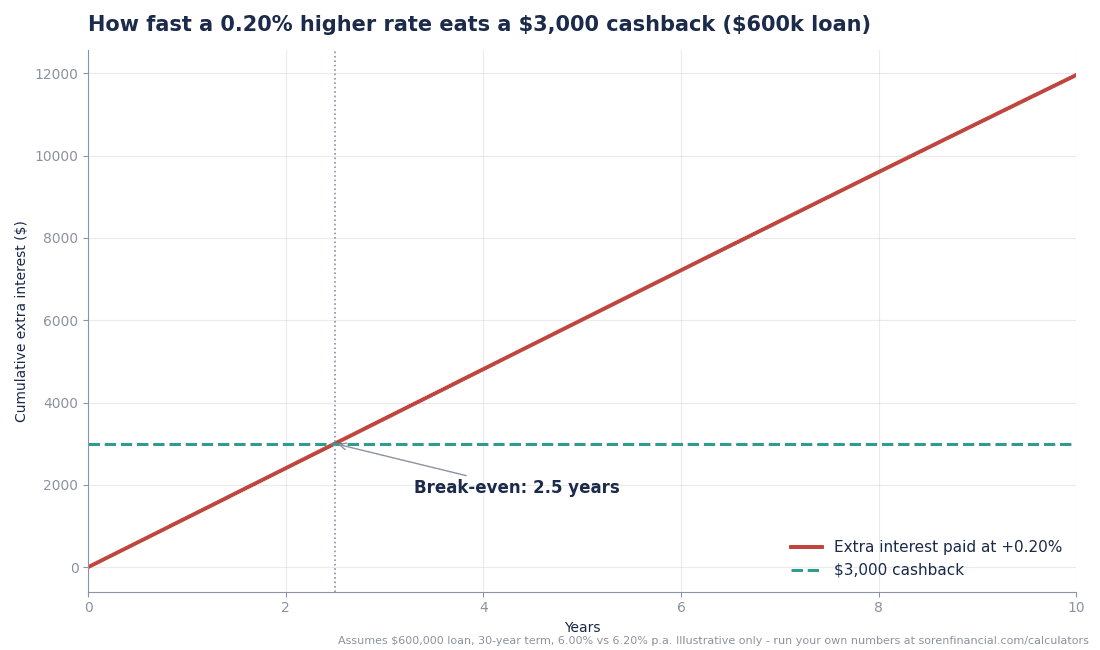

Ask your lender for their best rate for your LVR — in writing. Then compare it to the market. Lenders keep their best pricing for new customers, and the gap between what they offer loyal borrowers and what they offer strangers is the loyalty tax we bang on about in our refinancing tips. If they will not sharpen the pencil, a refinance with a clean file is straightforward — and a couple of lenders still pay cashbacks for it.

4. Re-run your budget at the new repayment before it hits

If you fixed at a low rate, your new repayment will be materially higher — run the number on our calculators before it lands, not after. If the new repayment does not fit, you have options while you still have time: extending the term for breathing room, restructuring, or consolidating other debts. All of them work better 3 months early than 3 missed payments late.

5. Decide your next structure like it is a new loan — because it is

Rolling off fixed is the natural moment to rethink everything: fix again, go variable with an offset, or split. Some lenders are currently pricing 2-year fixed below variable, and the OurTop10 Rate Prediction Index reads 77.7% hold / 22.3% hike for the 11 August meeting — the full fix-or-not framework is in is now the time to fix my home loan.

Moral of the story: a fixed rate ending is only a cliff if you walk it blind. Get in touch at startnow@sorenfinancial.com 3 months out and it becomes a step. Client reviews on OurTop10.

About the author

Mansour Soltani

Founder and CEO, Soren Financial

Mansour leads Soren Financial, working with clients across home loans, refinancing and property investment. A regular media contributor to ABC, Domain and Australian Broker, he holds a Certificate IV and Diploma in Finance and Mortgage Broking.

View full profile →